The Home Center Challenge - April 2007

By Santo Torcivia

Satchel Paige, the ageless baseball player, used to say “Don’t look back. Something may be gaining on you.” Although many people in the retail flooring business seem to be taking Satchel’s advice, good advice in baseball doesn’t always translate into good advice for business. In fact, there’s been something gaining on the flooring specialty store in the past decade—and they look like big boxes from here.

| HOW WE GOT THERE |

|

Before we lay out our statistics, we need to explain a few things so you'll understand the basis for our conclusions.

|

A lot of statistics are tossed around about the big boxes’ share of retail floorcovering sales. But most of them don’t compare apples to apples. They simply don’t look at direct competition between the home centers and independent floorcovering retailers.

You can’t know just how intense the competition has become until you look behind the basic numbers.

| RETAIL AND CONTRACT SHARES OF 2006 FLOORING SALES | ||||||

| Retail Channels |

Total |

Market Segments |

||||

|

Consumers/ |

Builder/ |

Commercial |

Commercial |

OEM & |

||

| Home Depot (1) Lowe's Menards |

10% 6% 0.4% |

15% 11% 0.7% |

7% 1% 0.1% |

5% 2% 0.2% |

0% 0% 0% |

0% 0% 0% |

| Major Home Centers Total All Other Home Center/Building Material |

17% 7% |

26% 10% |

8% 4% |

7% 13% |

0% 0% |

0% 0% |

| Total Home Centers Flooring Stores All Other Retail (2) Builder Flooring Contractors (3) Wood Flooring Contractors Ceramic Tile Contractors Commercial Flooring Contractors OEM & Manufactured Housing (4) Direct to End User (5) |

24% 35% 5% 5% 3% 7% 16% 2.9% 2.6% |

36% 45% 8% 0% 2% 6% 0% 0% 3.3% |

12% 38% 1% 31% 8% 8% 0% 0% 1.9% |

20% 50% 2% 10% 3% 12% 0% 0% 2.8% |

0% 0% 0% 0% 2% 7% 87% 0% 4% |

0% 0% 0% 0% 0% 0% 0% 100% 0% |

| Totals | 100% | 100% | 100% | 100% | 100% | 100% |

| The numbers above are for product sales only and exclude ceramic wall tile, rubber mats and runners, and all installation and related sales. (1) Home Depot figures include sales for its contractor sales division, HD Solutions. (2) All Other Retail includes the following store types: department and furniture stores, decorating stores, and all other retail outlets selling flooring but not shown separately. (3) Sales for Home Depot's builder flooring contractor division, HD Solutions, are shown with the company. (4) OEM & Manufactured Housing includes all mobile home, truck trailer, and other original equipment manufacturers (OEM) producing transport equipment and similar products. (5) Dire Sales to End Users includes non-store sales to all end users: consumers, builders, and commercial firms. These sales include catalog, Internet, 800 telephone, and any other sales purchased by end users direct from manufacturers. (6) All area rug sales are assumed to be Consumer/Residential Replacement market segment sales for this analysis. |

||||||

Last year, home centers accounted for 24% of the over $54 billion of retail flooring sold in the U.S., compared to 35% for specialty flooring stores. Even more dramatic, Home Depot and Lowe’s accounted for 16% of that 24%. Seen on the whole, flooring stores now account for only a little more than one third of U.S. flooring sales.

But those statistics don’t tell the real story about the head to head competition between specialty flooring retailers and home centers. If you’re a specialty retailer and you really want to know who’s gaining on you, it’s critical that you understand all the statistics.

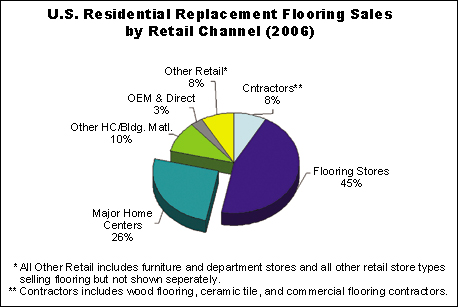

In the important and highly profitable residential replacement segment, the competition is getting much closer. Flooring stores represented 45% of the dollar value of all residential replacement flooring sold in 2006 in the U.S., versus 36% for all home centers. Home Depot and Lowe’s alone accounted for a combined 26% of flooring sold in that segment last year. That means that among consumers buying replacement floors for their homes, these two home center chains, which have 3,325 stores combined in the U.S., were doing 58% of the volume of the nation’s 14,000-plus flooring stores last year (see the chart below).

This startling statistic has significant implications for both sides in terms of supplier leverage, market sales and discipline, and ultimately cost.

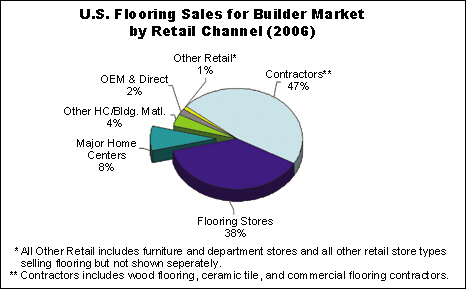

The builder market is another area where the specialty flooring store has been challenged, in this case by builder contractors, including Home Depot. In 2006, specialty flooring stores accounted for just 38% of all flooring dollar sales in the builder market segment, compared to builder contractors, who accounted for 47% of builder sales. (Among all contractors, builder flooring contractors represented 31% of U.S. sales to builders, while wood flooring and ceramic tile specialty contractors each accounted for 8% of the market.)

An important point to make here is that Home Depot owns the largest builder flooring contractor in the country, HD Supply. That firm alone accounted for 7% of all flooring sold to U.S. builders last year. HD Supply (whose flooring business is known as Creative Touch Interiors) is twice as big as the next biggest competitor. HD Supply’s sales are included in Home Depot figures, since it is wholly owned by that firm.

Commercial flooring contractors, also included in the contractor category, do not sell product to builders (see chart on page 30). These firms, which we refer to as Contract Dealers, sell to commercial projects in the corporate, healthcare, education, retail, hospitality, government and similar market sectors.

So we can see by the above numbers that the threat to the specialty flooring store posed by home centers, builder contractors and other competitors is formidable, even though we’re hearing a lot about Home Depot’s troubles these days. These competitors are always experimenting with new retail concepts and planning new ways to go to market.

Copyright 2007 Floor Focus

The independent flooring stores that are going to succeed will have to be planning ahead as well. Home centers and large chains have one significant advantage—they see potential flooring customers regularly when they come to their stores to purchase lawn equipment, lumber or light bulbs. Flooring stores need to invest some of their margin in advertising to keep in front of potential customers, since their stores don’t draw them in on a regular basis with other merchandise. Flooring retailers must continue to experiment with new merchandising systems and new media, and leverage their superior service advantage and product expertise into a creative and effective positioning for their stores. Retailers who belong to groups should use advertising co-op dollars effectively and often, and pressure their buying group or manufacturer’s retail group to invest in more advertising. (As we went to press, we learned that Carpet One dealers are going to be spending nearly 2% of their sales—some $75 million a year—on advertising.)

In 2005 Home Depot and Lowe’s spent an estimated 0.5% of sales on flooring advertising. (Proctor & Gamble, by the way, spends 8% of its sales on advertising.) How does your investment compare for your store? If you’re not spending more than 1% of your sales, you’re falling behind. You cannot afford to let the competition speak to your customers, especially your best customers, more frequently or more compellingly than you do.

Related Topics:The International Surface Event (TISE), Carpet One, Lumber Liquidators