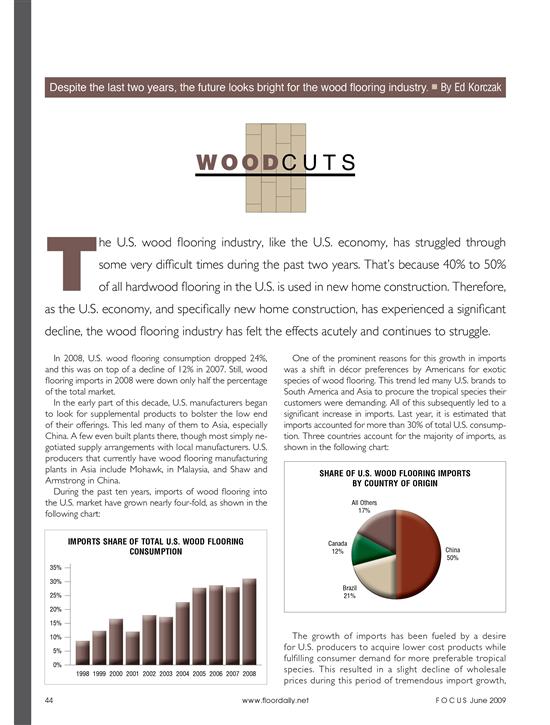

Wood Cuts - February 2011

By Ed Korczak

For years now, many industry analysts have reported doom and gloom scenarios about the specialty retail market. Some analysts have identified a trend in consumer spending that favors discount merchandisers like Walmart and Target, while specialty retailers like Nordstrom and Neiman-Marcus reported significant sales declines. The trend, of course, has been intensified during the past few years as a direct result of the current economic environment in the United States. Consumers are being much more conservative with their spending as job security remains questionable and the housing market continues to be uncertain.

The good news is that specialty retailers are here to stay. Overall sales may be down, but the Nordstroms of the world continue to thrive and meet the needs of a highly demanding and specialized market. These consumers may be buying their paper towels and toilet paper at a discount retailer, but they continue to favor specialty stores when it comes to higher ticket items that are not frequently purchased.

Current research also shows that consumers are changing the way they shop as well. Today, half the workforce in the United States is composed of women. Because women generally tend to be the primary shoppers for their families, shopping now is viewed as more of a chore than a relaxing afternoon outing. The bottom line is that women no longer have the time to shop that they once did. This means that consumers are spending less time participating in the act of shopping than they did just a few short decades ago. And in many cases, especially for high-dollar items like flooring, they are doing their legwork and research about the product online, using the Internet before they ever set foot in a retail store of any type.

In essence, there are primarily three types of consumers in the market today: those who are looking for the best price available; those who are looking for a full-service shopping experience; and, representing the vast majority of the consumer market, shoppers who are price conscious but also want value for their investment. And while this trend certainly is obvious for everyday items like household goods, clothing and food, it also applies to other purchases that are made less frequently, like furniture and flooring.

Flooring retailers have evolved in recent years to meet this demand in consumer spending habits. Home centers have grown dramatically during the past decade as consumers became more price conscious. According to the 2011 US FLOOReport, researched and compiled by Market Insights/Torcivia and Floor Focus, home centers represented about 10% of the total retail flooring market in 1997. Just ten short years later, in 2007, the total retail flooring marketshare for home centers had risen to more than 40%. This includes all types of flooring: wood, laminate, tile, stone, vinyl, rubber and carpet.

The success of home centers can be attributed to several factors. First, they provide consumers with convenience that other flooring retailers do not, because they offer so many housing related products and do it all under one roof. This addresses the time crunch problem consumers now face. Consumers can buy their flooring, light bulbs, and grass seed all in one convenient location, while waiting for their paint to be mixed.

Second, home centers also have the advantage of bulk buying power. Much of the success of home centers has been with the do-it-yourself market, as well as the cash and carry customer. These consumers are generally motivated by price. They are looking for the best deal and not a lot of customer service.

Finally, home centers have the distinct advantage of having multiple locations. In 1993, Home Depot and Lowe’s had 575 retail outlets combined. In 2009, they had 3,730 retail outlets between the two of them. These figures represent a nearly 650% increase in just over 15 years. To further illustrate this point, in 1993, Lumber Liquidators was not even recognized among the top 25 retail flooring outlets. In 2009, they were ranked third, following both Home Depot and Lowe’s, respectively.

Beyond convenience and price, home centers do not offer a lot more for their customers. Generally speaking, they do not offer installation services, and in fact, in June 2008, Home Depot announced that it was no longer focusing on installed flooring sales. This means that consumers are left to either install the flooring products they purchase themselves or find their own installers. The other downside to home centers is that they do not provide consumers with a great deal of selection. When it comes to hardwood, they generally offer prefinished products, in a small number of species, and in a limited number of sizes, widths, and formats. It is these two scenarios that give the specialty flooring retailers their biggest advantage.

In a customer satisfaction survey conducted by Floor Focus and Market Insights/Torcivia, consumers ranked specialty flooring stores as superior in installation expertise, product assortment, salesperson knowledge, salesperson assistance, store reputation and overall customer satisfaction. What specialty retailers offer consumers that home centers do not is customer service. Because specialty flooring stores focus on one category and one category only—flooring—they are able to offer their customers a very high level of personal service. The salespeople at these stores work with their customers to determine their specific flooring needs. For example, a home with three young children and a dog will have significantly different flooring needs from a home that has a retired couple with no pets. Salespeople in specialty retail stores also are extremely knowledgeable about the products they sell, and are better able to steer their customers toward products that will meet their needs, not just the salesperson’s personal sales quotas.

Specialty retail stores also tend to offer a much more diversified selection of products. For wood flooring alone, there are hundreds of wood species available in a veritable rainbow of colors and formats to achieve any design requirement. These species are often available in both prefinished and unfinished formats, in a variety of widths and thicknesses, as either solid or engineered wood, and offered in a variety of stains and finishes. There are literally limitless options available in specialty retailers that the home centers do not offer.

Another advantage of specialty stores is that they provide their customers with a full-service shopping experience. With a specialty retailer, consumers can easily include matching or custom floor vents with their flooring purchase. For wood floors in particular, the floor vents can be installed at the same time as the rest of the floor and can be a seamless transition in the floor, blending in with the flooring material to become a part of the actual floor itself. Matching and custom moldings are an option as well, making the final floor a truly coordinated part of the customer’s room décor.

Finally, specialty retailers typically do not just sell flooring material; they generally sell the installation services for the flooring material as well. In this way, consumers are not left to fend for themselves to find qualified flooring installers. By purchasing both the flooring material and the installation services from the same retailer, the purchaser can be assured that the end product will be guaranteed and that they will have a resource for any issues that may arise at a later date. Consumers will also have a place to turn to when the floor eventually needs to be refinished or updated.

The good news is that there is plenty of room in the flooring market for both home centers and specialty retailers, as well as everything in between. Each fills a unique niche for a very different clientele. Like the retail giants or the specialty retailer—including thousands of specialty flooring stores—the key is to know your customer, identify her needs, and do everything you can to meet and exceed those needs. Ultimately, that is the key to retail success.

Copyright 2011 Floor Focus

Related Topics:The International Surface Event (TISE), Lumber Liquidators